Turning Washington’s newest tax credit into a universal child benefit would make sure no child falls through the cracks.

This is our second blog post in our ongoing research collaboration series with a national progressive policy analyst, People’s Policy Project’s Matt Bruenig. Bruenig previously worked at Demos and the NLRB, and has been published and covered in the New York Times, Washington Post, and Vox. He is a frequent collaborator on welfare legislation with national progressive leaders such as Rep. Rashida Tlaib.

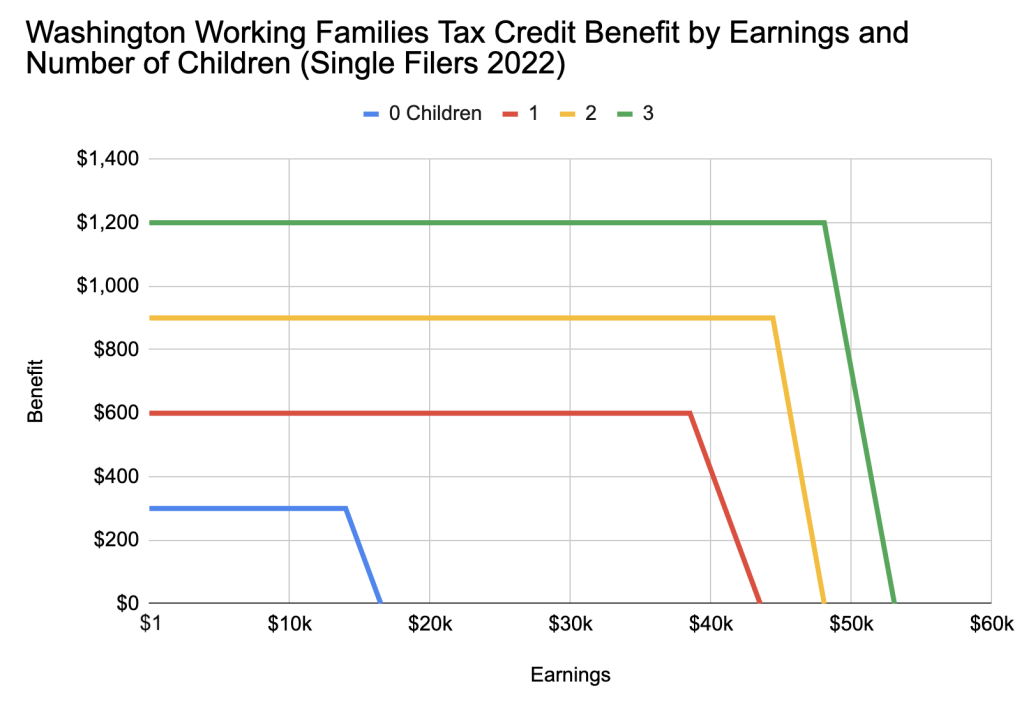

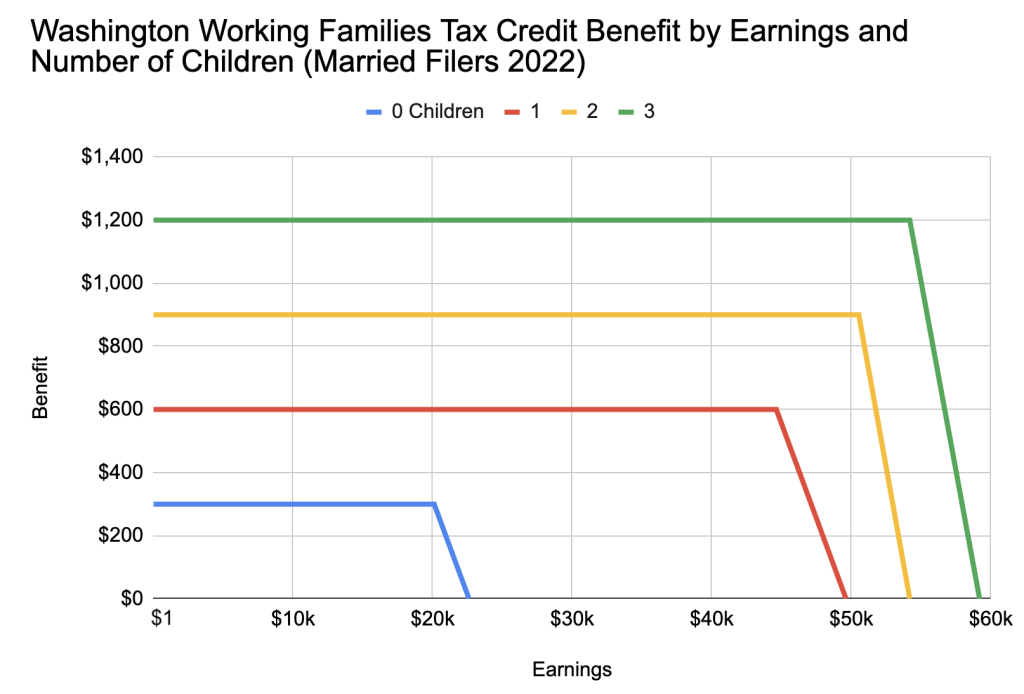

The Washington Working Families Tax Credit (WA WFTC) is widely considered to be one of Washington’s strongest economic and racial justice policies. After being passed in 2008, the program is finally set to launch this year and pay out cash benefits, up to $1,200, to potentially hundreds of thousands of Washington families. These much-needed funds can make the difference in keeping a roof over a family’s head or making sure children don’t go to school hungry.

A huge debt of gratitude is owed to the extraordinary coalition work of 46 diverse organizations, spanning from labor unions to domestic violence survivors’ advocacy groups, that pushed (and pushed!) legislators to fund the WFTC.

Despite many bright points, People Policy Project’s Matt Bruenig’s recent analysis shows the WFTC will exclude half of low-income children from the benefit, due to poor policy design. We don’t believe this exclusion was done intentionally or out of malice, rather, this is the result of common flaws in American welfare policy design, not unique to WA.

Bruenig outlines a path forward to an improved and universal WFTC, similar to the administrative design of Alaska’s Permanent Fund Dividend. We are ready to work hand in hand with our coalition partners in Washington to take up the important task of fixing the WFTC to not exclude hundreds of thousands of poor children and families.

The current WFTC policy design: good and bad

Beginning with the good, the WFTC is one of few state tax credit programs that is eligible to residents who file federal taxes using an Individual Tax Identification Numbers (ITIN). This enables the program to not exclude Washington’s undocumented immigrants, which is excellent.

The bad is the policy will exclude around half of low-income children. Bruenig explains:

“On first glance, the WA WFTC program appears to be designed to ensure that all Washingtonian children living in lower income families receive a few hundred dollars each year. But this will not happen for three reasons:

- Children living in families with $0 of earnings are not eligible for the WA WFTC benefits.

- Children living in families that do not file federal income tax returns are not eligible for WA WFTC benefits.

- Children living in families that fail to separately apply for the WA WFTC will not receive WA WFTC benefits.”

According to the Annual Social and Economic Supplement of the Current Population Survey (CPS ASEC), there were 1,786,000 children in Washington in 2021. Bruenig uses Census and IRS data to determine around 117,000 (6.5 percent) of those children lived in tax units that had no earnings. The data shows Black and Latino children are disproportionately overrepresented. The following graph shows what percentage of low-income children live in no earnings tax units out of all low-income kids. Bruenig defines kids as low-income if their family income is not too high to be ineligible for the EITC.

Bruenig continues to note that many Washington low-income families will be ineligible because they do not file federal income taxes.

“According to the IRS, 25.6 percent of Washingtonian families that are eligible for the federal EITC do not apply for it, typically because they do not file federal tax returns. This indicates that, in addition to the 26.6 percent of low-income kids who are too poor to receive the WA WFTC, another 18.8 percent of low-income kids will be ineligible for the program because their family does not file federal income taxes. Combined, these two exclusions will keep 45.4 percent of low-income kids out of the WA WFTC program.”

The final obstacle Bruenig notes is the fact that WA families will have to file a separate application to the Washington Department of Revenue with their federal tax filing to claim to the WFTC. Because Washington has no state income tax, it is not as simple as checking a box when filing state taxes.

“It’s hard to say for sure how many people will fail to jump through this hoop, but if the participation rates of other welfare programs are any indicator, the number will be substantial. If we assume very conservatively that only 10 percent of people will fail this hurdle, then that knocks another 5.5 percent of low-income kids out of the WA WFTC program, bringing the combined total to one in two low-income kids.”

The solution: a well-designed universal program

As detailed above, the current WFTC design is untenable for reasons of economic and racial justice. So, how can we design a policy that reaches its target population: low-income children and families of all races?

Bruenig suggests a simple and elegant solution, a universal benefit with an administrative framework similar to Alaska’s Permanent Fund Dividend (PFD). Bruenig suggests calling the universal benefit the Washington Child Benefit, but it could just as easily continue to be called the Washington Working Families Tax Credit. (Whatever is more politically expedient.)

The universal benefit would pay a single and flat amount to every child resident and would be funded by a payroll tax. For example, a one percent payroll tax applied to the QCEW base would generate $2.77 billion of revenue, enough to provide $1,548 to all 1,785,000 children in the state.

The application process would be simpler than the current WFTC one. Residents do not need to prove their income or file federal taxes—they would only need to certify their residency similar to the PFD.

Bruenig concludes by addressing what is likely to be a common objection: isn’t a universal program wasteful and inefficient because it also gives a benefit to wealthy families?

“But this is a mistaken understanding of how these benefits work. The amount someone would (net) benefit from the scheme described above is equal to the amount they receive from the child benefit minus the amount they pay in the payroll tax. The lowest income people will pay no payroll tax and thus receive the most (net) benefit. As you move up the earnings scale, the child benefit amount stays the same, but the payroll tax amount rises, driving the (net) benefit down. Thus, such a scheme actually provides (net) benefits that are directly proportional to income, with the bottom receiving the most, and the top receiving the least (indeed the top actually pays more in tax than they receive in child benefits).

In general, this kind of “universal” design is superior to the typical “means-tested” design that tries to use each person’s income to determine what their benefit payment should be. But this is especially true in the case of Washington where the lack of a state income tax means that it simply does not have the administrative ability to cleanly execute a means-tested tax credit.”

Washington State has an important role to play in providing residents and communities with a solid foundation to build on for a good life. Let’s work together to fix the WFTC with a simpler, universal benefit that will set our children and families up for success.